As an EPF contributor and tax payer, I am most perplexed and worried by this latest pre- general election allocation of our statutory life savings.

Showing posts with label Financial Analysis. Show all posts

Showing posts with label Financial Analysis. Show all posts

Sara Rakyat 1M, AS1M and national debt?

The latest BN flagship roll out in election year is the attention grabbing Sara Rakyat 1Malaysia which is already very well explained in this post.

Kudos to the analyst for such an insightful piece of writing!

A responsible and proper government should be giving its people an environment where they can get good employment and business opportunity, clean and efficient governance. A responsible government should not be telling the deprived segment of population to borrow money and engage in equity investments.

The key selling point by BN administration is guaranteed return. No unit trust or investment manager in the world would dare to guarantee returns on investment.

Besides, if one is earning between RM500 to RM3,000, how much surplus that individual or family can afford to borrow and invest? They probably need a job and a fixed salary more, not some investments which pays a token RM50 a month but not immediately usable for buying household goods

Anyway, intrigued by the promise of “guaranteed return” I decided to find out more about this matter.

Is it really better off under BN than Pakatan?

It is customary for us to be lectured to be grateful to BN as they are the only one who can safeguard Malaysians’ well being.

------------------------------------------------------------------------------------------------------

SEREMBAN, Oct 15 — Tan Sri Muhyiddin Yassin told Malaysians today to be grateful to the Barisan Nasional (BN) government for its many efforts which have improved their lives.

……………………

He urged the Ampangan folk against following in the footsteps of people from Selangor and opposition-held states who voted for the opposition during Election 2008.

“It’s not easy to be the government; the opposition is only good at making promises which they never have to fulfil,” he was quoted as saying in Bernama Online.

Budget is also a form of a promise, i.e. a promise to deliver at a predetermined planned price. BN’s ability to fulfill promises is also open to scrutiny as we can see so many mega cost overruns whether it is for Bakun Dam, KLIA 2, PKFTZ or the new palace.

Let's not talk about all those surpluses in Pakatan administered states for now.

I went to Jabatan Statistik Negara to evaluate the DPM cum Education Minister’s claim and come up with some interesting statistics.....

National debts: more puzzling numbers tumblin'

Recently there is a claim in this video, MalaysiaYouth4Change that according to a report on 13th Jan 2011 by Thompson Reuters Eikon, the bonds sold by Malaysia national debt is USD179 billion which' at optimistic exchange rate of RM3 to USD1, is a whopping RM537 billion, very much higher than RM271 billion as at June 2010 as reported the finance ministry.

I have no idea how TRE derived the number and baffled by the huge gap between this number and the finance ministry figures, on which the Prime Minister had cheerfully advised Malaysians that national debts have decreased.

Then some curious person sent me the breakdown of TRE numbers hoping I could clarify the situation. I am amused by this because I am certainly not part of the federal finance ministry administration but I can just take a cursory look at the data and hope to point out a thing or 2.

Picture 1 shows the finance ministry number as at 30 June 2010

Picture 2 shows the Thompson Reuters Eikon numbers, very much higher

Picture 3 shows some more detailed information

Luckily there is an excel file which makes analysing easier

Base on a cursory review of the 2 sets of data, the discrepancies could be explained by

1) Finance Ministry only included bonds issued to Malaysia where as TRE included bonds issued to proxies such as Petronas, Khazanah, MISC etc

2) that still leaves a sizable difference between the TRE and finance ministry numbers - it could be different exchange rates applied and also classification differences between these 2. Statistic collection can be a dodgy business.

In any case, the Malaysian government should seek to clarify this with TRE urgently because its figure is giving a different impression from what the finance ministry is giving, hence confusing the business communities, foreign and local, as well as all tax payers.

Not to mention it cast doubt on the integrity and competence of the present administration.

The last time when a leading Malaysian official dismissed an analyst's report, the rebuttal from the foreign investor community harmed all Malaysians. (Remember the DPM and PERC issue?)

The graph below summarise the differences between the 2 sets of numbers.

The bonds carry some abstract description that looks like the name of borrower. I just did a "match, guess and hope for the best" and made a best guess hear: looks like about RM36 billion under Khazanah, RM48 billion under Petronas, RM5 billion under MISC, RM6 billion under KLIA.....

Note the huge jump in bonds issued since June 2010?

I blogged about this last year

"According to Singapore's Today, Dow Jones reported that 21 more government bonds auctions (really it means rakyat debts committed by temporary administrators on their behalf without getting rakyat's consent), 1/3 more than this year, to raise money to spend on 131 "key projects" (which should include the much objected Menara Warisan Merdeka).

Malaysians are expected to owe another RM90 billion from debts raised in 2011 alone; the years and years of accumulated debts as at 2008 alone was already RM213 billion.

In 2011, Najib's administration will almost double our debts and subject us to more foreign exchange risks. The loans are for infrastructure and property projects - not a whimper about healthcare, human capital development, education .... the soft skills so vital nowadays and Malaysians so lack of it nowadays."

Also, the finance ministry must clarify their methodology of reporting national debt figures to the general public. At the moment, it seems to me that whenever "national debts" is discussed, it only involves bonds issued to Malaysian government, and it excludes Hutang Dalam Negeri Kerajaan Persekutuan (the bulk of it includes KWSP & all those sijils in your hands bought by your savings) and the burden carried "special purpose vehicles" which some accounts are not for public scrutiny, like Khazanah and Petronas.

Otherwise it looks like Off Balance Sheet finance/debts carried at somewhere else to me, a term that makes ex-Enron pension holders cringe with despair.

I have no idea how TRE derived the number and baffled by the huge gap between this number and the finance ministry figures, on which the Prime Minister had cheerfully advised Malaysians that national debts have decreased.

Then some curious person sent me the breakdown of TRE numbers hoping I could clarify the situation. I am amused by this because I am certainly not part of the federal finance ministry administration but I can just take a cursory look at the data and hope to point out a thing or 2.

Picture 1 shows the finance ministry number as at 30 June 2010

Picture 2 shows the Thompson Reuters Eikon numbers, very much higher

Picture 3 shows some more detailed information

Luckily there is an excel file which makes analysing easier

Base on a cursory review of the 2 sets of data, the discrepancies could be explained by

1) Finance Ministry only included bonds issued to Malaysia where as TRE included bonds issued to proxies such as Petronas, Khazanah, MISC etc

2) that still leaves a sizable difference between the TRE and finance ministry numbers - it could be different exchange rates applied and also classification differences between these 2. Statistic collection can be a dodgy business.

In any case, the Malaysian government should seek to clarify this with TRE urgently because its figure is giving a different impression from what the finance ministry is giving, hence confusing the business communities, foreign and local, as well as all tax payers.

Not to mention it cast doubt on the integrity and competence of the present administration.

The last time when a leading Malaysian official dismissed an analyst's report, the rebuttal from the foreign investor community harmed all Malaysians. (Remember the DPM and PERC issue?)

The graph below summarise the differences between the 2 sets of numbers.

The bonds carry some abstract description that looks like the name of borrower. I just did a "match, guess and hope for the best" and made a best guess hear: looks like about RM36 billion under Khazanah, RM48 billion under Petronas, RM5 billion under MISC, RM6 billion under KLIA.....

Note the huge jump in bonds issued since June 2010?

I blogged about this last year

"According to Singapore's Today, Dow Jones reported that 21 more government bonds auctions (really it means rakyat debts committed by temporary administrators on their behalf without getting rakyat's consent), 1/3 more than this year, to raise money to spend on 131 "key projects" (which should include the much objected Menara Warisan Merdeka).

Malaysians are expected to owe another RM90 billion from debts raised in 2011 alone; the years and years of accumulated debts as at 2008 alone was already RM213 billion.

In 2011, Najib's administration will almost double our debts and subject us to more foreign exchange risks. The loans are for infrastructure and property projects - not a whimper about healthcare, human capital development, education .... the soft skills so vital nowadays and Malaysians so lack of it nowadays."

Also, the finance ministry must clarify their methodology of reporting national debt figures to the general public. At the moment, it seems to me that whenever "national debts" is discussed, it only involves bonds issued to Malaysian government, and it excludes Hutang Dalam Negeri Kerajaan Persekutuan (the bulk of it includes KWSP & all those sijils in your hands bought by your savings) and the burden carried "special purpose vehicles" which some accounts are not for public scrutiny, like Khazanah and Petronas.

Otherwise it looks like Off Balance Sheet finance/debts carried at somewhere else to me, a term that makes ex-Enron pension holders cringe with despair.

Part II shadow national debts and other obligations

Last week, after pointing out the relatively obvious Hutang Dalam Negeri Kerajaan Persekutuan that was not commented in PM’s trumpet blowing, the trick is to identify where else our liabilities are hidden.

Firstly, some economics 101:

Public goods – goods and services that should preferably be provided by public sector rather than private entrepreneurs at no profit. It is a social responsibility to ensure equity (fairness) in a free economy market. Traditionally these items are provided by the state from tax payers’ contribution for the common good where the rich subsidise the poor and not at a profit. Examples of such goods and services are public roads, utilities, postal services, health and education services.

Another reason is that it is not practical for private sector to provide such services e.g. police and security forces. (Although Malaysian defense contracts have famous ways – all the way to France - of going about such things)

In Malaysia, Mahathir administration started an irreversible tsunami of privatization like Indah Water, Tenaga, Telekon, Alam Flora etc. One argument is that corporate taxes is lowered by such privatization because the government is relieved of its duty to provide them.

Fine, then how come successive Badawi and Najib administrations have tried so hard to widen tax collection via GST, raised the service tax percentages and introduced credit card taxes?

I have taken a cursory examination of hidden national debts as a result of the above mentioned privatization trend. If a good or service was and still can be provided by the state at no profit, and this function has been taken over by private sector, then borrowings incurred by these companies are repaid by consumers who have no choice but continue to purchase these goods and services.

Base on the limited research I could do with published audited accounts and common knowledge, I have identified some well known private companies who took over various state functions at a profit and incurred borrowings.

Some of them are self explanatory and obvious like Pos Malaysia, Tenaga and Telekom. Proton is something that Mahathir should never tried in the first place but we have to pay for it while Ahmad Zaki Berhad gets most of their revenue from JKR projects, Faber Group are steep in health care, facilities management of LRT while KUB’s role is revealed further below.

Base on my previous articles, PAAB and MyEG are probably going to increase their borrowings very significantly to RM20 billion and RM100 million respectively.

In the extreme case of Plus, in 2009, the dividend it paid shareholders amounted to some RM800 million, equal to the amount of “compensation” paid by the Barisan Nasional administration on our behalf.

Take a look at the level of retained earnings kept in the fat pockets of my selected samples and the level of retained profits/fats in Proton make my stomach churn.

Below: why do we need to pay so that these chaps below can have such a big piggy bank? (the numbers are in RM'000)

And in cases of non-listed privatization, the general public will never know the true extend of the amounts involved.

I am not against private entities taking a risk, make a profit and provide job opportunities but I am against excessive profits derived from sheltered crony dominated environment. Lee Kuan Yew told the chief of Singapore Airline upon commencement of operations that he either make profit within 3 years or get shut down hence SIA become an internationally reputed airline...the same can not be said about MAS.

Being a listed company with shares also means it can be bought and sold unlimited times and every time when some one purchased a company with multi million deals, such investments (and interest on borrowings) would have to be repaid, hence the cost of goods and services would have to be raised, again.

------------------------------------------------------------------------------------

http://wangsamajuformalaysia.blogspot.com/2010/11/tradewinds-m-berhad-your-rice-and-sugar.html

2. Material Contracts Involving Directors and Major Shareholders

(a) a Share Sale agreement dated 28 august 2009 between Tradewinds (M) Berhad (“TWS” or the “Company”) and Wang Tak Company Limited (“WT”) for the acquisition of 148,281,100 ordinary shares of RM1.00 each in padiberas Nasional Berhad (“Bernas”), representing 31.52% of the total issued and paid-up share capital of Bernas from WT for a total purchase consideration of RM308,424,688.00. The said acquisition was completed on 2 November 2009.

----------------------------------------------------------------------------------

Why can’t we tax payers just pay some dedicated civil servants to be at their station and retire at their jobs, avoid paying for all the above? If the civil servants love their country, they should be able to provide adequate service and negate the nonsense about a profit crazy private entity always do better than civil servants.

Then again, if we talk about the civil servants' attitude moulded by more than 50 years of Alliance /BN administration, then it is another can of worms.

------------------------------------------------------

http://www.themalaysianinsider.com/malaysia/article/civil-service-inept-and-pro-umno-us-envoys-told

“Govindan sees Malaysia’s huge and largely ethnic Malay civil service, completely loyal to Umno, but increasingly incompetent, as PM Najib’s largest obstacle.

“He commented that the civil service has a very narrow worldview and will oppose, even refuse to implement, reforms perceived as damaging ethnic Malay interests, even if convinced of the long-run gains for Malaysia,” it said.

-------------------------------------------------------------------

And base on this exclusive here about KUB, dividends and further burden on rakyat do come hand in hand:

--------------------------------------------------------------------------

http://www.merdekareview.com/bm/news.php?n=11954

Polisi dividen: Petanda UMNO-BN semakin kesempitan wang?

Neo Chee Hua Jun 16, 2011 05:36:13 pm

KUB Malaysia Bhd yang mempunyai hubungan rapat dengan UMNO dan Kementerian Kewangan memaklumkan pada 14 Jun 2011, bahawa syarikatnya merancang untuk melaksanakan polisi dividen mulai tahun 2013 - ….

….., dua pemegang saham terbesar KUB Malaysia Bhd adalah Gaya Edisi Sdn Bhd (29.62%) dan Kementerian Kewangan (22.55%). ….. pemegang saham terbesar Gaya Edisi Sdn Bhd adalah Temasek Padu Sdn Bhd, dan Temasek Padu kini adalah pemegang harta parti pemerintah terbesar, UMNO.

Najib Razak telah menstruktur semula harta parti UMNO setelah mengambil alih tampuk pimpinan. Harta UMNO telah dimasukkan ke bawah Temasek Padu, dan syarikat ini dikuasai oleh orang rapatnya, Zulkifly Rafique, pengasas firma guaman Zul Rafique & Partners, dan seorang lagi peguam dari firma guaman ini, Tunku Alizan Raja Muhammad Alia.

Seandainya KUB Malaysia Bhd melaksanakan polisi dividen pada tahun 2013, ….. UMNO dan Kementerian Kewangan akan mendapat dividen pada kadar yang tetap dari KUB Malaysia Bhd setiap tahun.

….. KUB Malaysia dijangka bakal mendapat satu projek hospital kepakaran kanak-kanak yang bernilai RM3 bilion bersama IJM Corporation Bhd. Di bawah kontrak yang sama, KUB Malaysia bersama IJM bakal mendapat kontrak konsesi untuk mengendalikan hospital tersebut selama 30 tahun.

…. KUB Malaysia juga berniat untuk mendapatkan projek pembinaan lapangan terbang antarabangsa Kuala Lumpur kedua, yang bernilai RM250 juta, termasuk pembinaan landasan kapal terbang ketiga dan landasan teksi.

.... syarikat joint venture antara KUB Malaysia Bhd dengan Malaysia Steel Works (KL) Bhd juga berjaya mendapat satu projek inter-city commuter train bernilai RM1.23 bilion di bawah Wilayah Pembangunan Iskandar Malaysia.

-------------------------------------------------------------------------

Another interesting example is found within Ahmad Zaki Berhad. Take a look at the notes to accounts no 44 for year ended 31 December 2010.

We all know about the hoo haa about no open tender and non-competitive bidding and bail outs waste of public fund,

Point a) and point c) quite clearly indicate the performance of the Company is not satisfactory and yet point b) clearly also shows a direct award of further project funded by tax payers to this company. Surely there are other more competitive bumi contractors around?

We will never ever know, the true extent of how much we tax payers really owe.

Firstly, some economics 101:

Public goods – goods and services that should preferably be provided by public sector rather than private entrepreneurs at no profit. It is a social responsibility to ensure equity (fairness) in a free economy market. Traditionally these items are provided by the state from tax payers’ contribution for the common good where the rich subsidise the poor and not at a profit. Examples of such goods and services are public roads, utilities, postal services, health and education services.

Another reason is that it is not practical for private sector to provide such services e.g. police and security forces. (Although Malaysian defense contracts have famous ways – all the way to France - of going about such things)

In Malaysia, Mahathir administration started an irreversible tsunami of privatization like Indah Water, Tenaga, Telekon, Alam Flora etc. One argument is that corporate taxes is lowered by such privatization because the government is relieved of its duty to provide them.

Fine, then how come successive Badawi and Najib administrations have tried so hard to widen tax collection via GST, raised the service tax percentages and introduced credit card taxes?

I have taken a cursory examination of hidden national debts as a result of the above mentioned privatization trend. If a good or service was and still can be provided by the state at no profit, and this function has been taken over by private sector, then borrowings incurred by these companies are repaid by consumers who have no choice but continue to purchase these goods and services.

Base on the limited research I could do with published audited accounts and common knowledge, I have identified some well known private companies who took over various state functions at a profit and incurred borrowings.

Some of them are self explanatory and obvious like Pos Malaysia, Tenaga and Telekom. Proton is something that Mahathir should never tried in the first place but we have to pay for it while Ahmad Zaki Berhad gets most of their revenue from JKR projects, Faber Group are steep in health care, facilities management of LRT while KUB’s role is revealed further below.

Base on my previous articles, PAAB and MyEG are probably going to increase their borrowings very significantly to RM20 billion and RM100 million respectively.

My very crude calculation is that every Malaysian is saddled with RM1,750 worth of national debt hosted by private companies which are basically more costly government function. This debt can increase up to RM2,228 per person, excluding interest and related professional charges associated with huge syndicated borrowings such as legal fees, consultancy fees and bank charges.

I have barely scratched the surface. Further hidden from the public are examples like Indah Water Konsortium, Puspakom (which is consolidated under MRCB), Pharmaniaga etc as well as those sendirian berhads functioning as custodian of UMNO’s business interest like Temasek Padu Sdn Bhd.

Maybe readers out there can add onto the list like UEM, Peremba, Gamuda, Prasana, Alam Flora etc. It is endless and quite frightening to think about it.

Without a change of federal government, there is no way to get most of the picture out for public scrutiny and examination.

Price of goods and services the man and woman in the street have to pay for needs to cover the fat executive salaries*, principal and interest of the hidden nation debts, compliance cost of a listed company, market-base salaries with no retrenchment, advertisement costs, rent seekers (like the IPPs) so that the companies will have enough money to pay dividends and re-invest.

* example of Tenaga's director remuneration (click on the pix for a better view & see how much a director can get and see how many directors they have...do we need so many of them?) :

Privatisation also means the profits of the companies are taxed so in fact Malaysians are actually being taxed at a higher level as these companies have to factor in corporate taxes in their pricing structure.

All the above would actually more than offset cost of the previous structure where civil servants who are entitled to pensions but considerably less salaried and there is no profit and no corporate tax.

To illustrate what I am trying to say, see below:

In the extreme case of Plus, in 2009, the dividend it paid shareholders amounted to some RM800 million, equal to the amount of “compensation” paid by the Barisan Nasional administration on our behalf.

Take a look at the level of retained earnings kept in the fat pockets of my selected samples and the level of retained profits/fats in Proton make my stomach churn.

Below: why do we need to pay so that these chaps below can have such a big piggy bank? (the numbers are in RM'000)

And in cases of non-listed privatization, the general public will never know the true extend of the amounts involved.

I am not against private entities taking a risk, make a profit and provide job opportunities but I am against excessive profits derived from sheltered crony dominated environment. Lee Kuan Yew told the chief of Singapore Airline upon commencement of operations that he either make profit within 3 years or get shut down hence SIA become an internationally reputed airline...the same can not be said about MAS.

Being a listed company with shares also means it can be bought and sold unlimited times and every time when some one purchased a company with multi million deals, such investments (and interest on borrowings) would have to be repaid, hence the cost of goods and services would have to be raised, again.

------------------------------------------------------------------------------------

http://wangsamajuformalaysia.blogspot.com/2010/11/tradewinds-m-berhad-your-rice-and-sugar.html

2. Material Contracts Involving Directors and Major Shareholders

(a) a Share Sale agreement dated 28 august 2009 between Tradewinds (M) Berhad (“TWS” or the “Company”) and Wang Tak Company Limited (“WT”) for the acquisition of 148,281,100 ordinary shares of RM1.00 each in padiberas Nasional Berhad (“Bernas”), representing 31.52% of the total issued and paid-up share capital of Bernas from WT for a total purchase consideration of RM308,424,688.00. The said acquisition was completed on 2 November 2009.

----------------------------------------------------------------------------------

Why can’t we tax payers just pay some dedicated civil servants to be at their station and retire at their jobs, avoid paying for all the above? If the civil servants love their country, they should be able to provide adequate service and negate the nonsense about a profit crazy private entity always do better than civil servants.

Then again, if we talk about the civil servants' attitude moulded by more than 50 years of Alliance /BN administration, then it is another can of worms.

------------------------------------------------------

http://www.themalaysianinsider.com/malaysia/article/civil-service-inept-and-pro-umno-us-envoys-told

“Govindan sees Malaysia’s huge and largely ethnic Malay civil service, completely loyal to Umno, but increasingly incompetent, as PM Najib’s largest obstacle.

“He commented that the civil service has a very narrow worldview and will oppose, even refuse to implement, reforms perceived as damaging ethnic Malay interests, even if convinced of the long-run gains for Malaysia,” it said.

-------------------------------------------------------------------

And base on this exclusive here about KUB, dividends and further burden on rakyat do come hand in hand:

--------------------------------------------------------------------------

http://www.merdekareview.com/bm/news.php?n=11954

Polisi dividen: Petanda UMNO-BN semakin kesempitan wang?

Neo Chee Hua Jun 16, 2011 05:36:13 pm

KUB Malaysia Bhd yang mempunyai hubungan rapat dengan UMNO dan Kementerian Kewangan memaklumkan pada 14 Jun 2011, bahawa syarikatnya merancang untuk melaksanakan polisi dividen mulai tahun 2013 - ….

….., dua pemegang saham terbesar KUB Malaysia Bhd adalah Gaya Edisi Sdn Bhd (29.62%) dan Kementerian Kewangan (22.55%). ….. pemegang saham terbesar Gaya Edisi Sdn Bhd adalah Temasek Padu Sdn Bhd, dan Temasek Padu kini adalah pemegang harta parti pemerintah terbesar, UMNO.

Najib Razak telah menstruktur semula harta parti UMNO setelah mengambil alih tampuk pimpinan. Harta UMNO telah dimasukkan ke bawah Temasek Padu, dan syarikat ini dikuasai oleh orang rapatnya, Zulkifly Rafique, pengasas firma guaman Zul Rafique & Partners, dan seorang lagi peguam dari firma guaman ini, Tunku Alizan Raja Muhammad Alia.

Seandainya KUB Malaysia Bhd melaksanakan polisi dividen pada tahun 2013, ….. UMNO dan Kementerian Kewangan akan mendapat dividen pada kadar yang tetap dari KUB Malaysia Bhd setiap tahun.

….. KUB Malaysia dijangka bakal mendapat satu projek hospital kepakaran kanak-kanak yang bernilai RM3 bilion bersama IJM Corporation Bhd. Di bawah kontrak yang sama, KUB Malaysia bersama IJM bakal mendapat kontrak konsesi untuk mengendalikan hospital tersebut selama 30 tahun.

…. KUB Malaysia juga berniat untuk mendapatkan projek pembinaan lapangan terbang antarabangsa Kuala Lumpur kedua, yang bernilai RM250 juta, termasuk pembinaan landasan kapal terbang ketiga dan landasan teksi.

.... syarikat joint venture antara KUB Malaysia Bhd dengan Malaysia Steel Works (KL) Bhd juga berjaya mendapat satu projek inter-city commuter train bernilai RM1.23 bilion di bawah Wilayah Pembangunan Iskandar Malaysia.

-------------------------------------------------------------------------

Another interesting example is found within Ahmad Zaki Berhad. Take a look at the notes to accounts no 44 for year ended 31 December 2010.

We all know about the hoo haa about no open tender and non-competitive bidding and bail outs waste of public fund,

Point a) and point c) quite clearly indicate the performance of the Company is not satisfactory and yet point b) clearly also shows a direct award of further project funded by tax payers to this company. Surely there are other more competitive bumi contractors around?

We will never ever know, the true extent of how much we tax payers really owe.

Pos Malaysia : worth the fuss to privatise?

When Pos Malaysia was listed as a public limited company, it baffled me. Why bother privatising a monopoly? Remove the profit element and instill healthy working culture, and Malaysians can be spared the profiteering increase of postage from RM0.30 to RM0.70.

If privatisation is to provide more efficient service then the excellent article below spelt out the less than ideal situation beneath the exciting images portrayed by Pos Malaysia for the past few years.

In addition to the crippling Transmile Group scandal which whacked RM200-RM300 million off the profits of Pos Malaysia, the article also highlighted that its chairman and managing director had resigned over irregularities in land sales and award of contracts.

http://business.feedfury.com/content/17725759-pos-malaysia-new-scandal-after-transmile-irregularities.html

The fact that the chairman and managing director (bumiputras, no less) could only resign* in protest suggested that there were higher powers at work that frustrated & probably prevented capable and honest professionals from taking the necessary corrective action.

This kind of working environment will deter high calibre overseas based Malaysians from coming back. This is more important than the 15% income tax abruptly announced by Najib of which the details have yet to be worked out.

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

*foot note:

Very recently, the chairman took Pos Malaysia and Khazanah to court for breach of chairmanship contract.

http://www.sun2surf.com/article.cfm?id=60169

In the first suit, Adam is suing the Minister of Finance, the government and Pos Malaysia Bhd. In the second suit, which was filed separately, he named Khazanah Nasional Berhad managing director Tan Sri Azman Mokhtar as the defendant.

Adam told Bernama that his suit against Pos Malaysia had been settled amicably after he withdrew his legal action against it about three months ago.

- perhaps Pos Malaysia has to make peace knowing court action may not be advisable for them?

In the suit against Azman filed on Nov 4 last year, Adam alleged that due to unlawful interference by Azman, the government decided to terminate his contract through two letters signed by the Minister of Finance dated May 23 and May 26, 2008 whereas his appointment was supposed to end only on Feb 28, 2009.

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

Yeah sure those are old stories dated 2008 but let's look at the audited accounts for 2010:

Pos Malaysia invested RM7.6 million into 3 associated companies, of which are all wiped out as useless investment, worth RM0. Of the 3, Elpos Print Sdn Bhd earned a revenue of RM12.5 million, but as its liabilities greater than its assets and even whole year's revenue, something is wrong. (Imagine you owe loans and debts which exceed your whole year salary...that is terrifying or down right stupid financial management)

If you look at the notes for related party transactions, Pos Malaysia gave Elpos Print Sdn Bhd RM10 million revenue out of its RM12 million...so how can a small company given a fat contract with a national monopoly can end up being debt ridden up to such a mess?

Elpos Print Sdn Bhd is 60% owned by Econlink Sdn Bhd and Pos Malaysia owns the remaining 40%.

According to Pos Malaysia's website here,

----------------------------------------------------------------------------

http://www.pos.com.my/websitebm/main2.asp?c=/WebsiteBM/subsidiaries/Elpos.htm

Elpos Print Sdn Bhd merupakan salah satu daripada pencetak utama untuk Pos Malaysia Berhad. Elpos ditubuhkan secara perkongsian di antara Pos Malaysia Berhad dan Econlink Sdb Bhd pada tahun 1997.

----------------------------------------------------------------------------

One would expect Pos Malaysia, in awarding what is effectively a public service subcontract, would exercise caution and chosen a reputable party to be prudent with public funds.

A reputable company should exhibit some healthy form of publicity, so as to project a positive image and provide relevant information to advertise itself. Many SMEs have their informative and sometimes interactive website to facilitate ease of business.

Yet, when an attempt to google up this concessionaire, all I get is a scanty picture below:

The company does not own a website, like many SMIs, to let potential customers get to know about basic facts of the company like who are the board of directors, catalogue of their products and services etc. For a company that has been a concessionaire of Pos Malaysia since the last century, surely there should be enough accumulated profits, expertise, track record to be a successful and independent enterprise.

Yet I only see a relatively subdued enterprise named as "pencetak utama" by Pos Malaysia being written off as an investment despite getting a secured and relatively sizeable source of income from Pos Malaysia. It is also contradictory for Pos Malaysia to call it a key supplier and a useless investment simultaneously. Frankly when you are getting a secured, multi-million contract doing printing work for a monopoly cum glc, it is very very hard to run your company into deep shit unless you are supremely unlucky or incompetent.

Sure, in light of the multi million and multi billion ringgit scandals that numb Malaysians into oblivion, the above seems like a small matter but yet, if Pos Malaysia that has been in operations for decades can't even do simple things right, then we can forget about becoming developed nation, Vision 2020, High Income Nation and all the other sales pitch for election

The lastest about Pos Malaysia though, is the disposal of Pos Malaysia by Khazanah to Syed Mokhtar

---------------------------------------------------------------------------

http://www.todayonline.com/Business/EDC110423-0000325/DRB-to-buy-Msian-govts-stake-in-Pos-Malaysia

DRB to buy M'sian govt's stake in Pos Malaysia

04:46 AM Apr 23, 2011

KUALA LUMPUR - DRB-Hicom, a Malaysian automotives, construction and banking group controlled by billionaire Syed Mokhtar Al Bukhary, has won a race to become the biggest shareholder in the Malaysia's national postal company.

It will pay RM622.8 million (S$255.6 million), or RM3.60 per share, for a 32.2-per-cent stake in Pos Malaysia, according to an e-mailed statement by Khazanah Nasional yesterday. That is a 7-per-cent premium to the company's closing share price yesterday of RM3.37.

Khazanah, an investment arm of the Malaysian government, is divesting after Prime Minister Najib Razak called on state organisations to sell down some non-core local commercial holdings to help boost stock market liquidity and attract investment. DRB-Hicom beat four other rival bids which Khazanah did not name in the statement.

----------------------------------------------------------------

In evaluating the bid from various parties, Najib administration awarded the sale to Syed Mokhtar base on the following argument:

"DRB-Hicom was chosen based on their overall bid, which offers not only a defined strategy but also an executable business plan and an acceptable offer price," Mr Azman Mokhtar, managing director of Khazanah....

I have previously written that according to the 2009 audited accounts of Tradewinds (M) Berhad (TW), TW sold sugar, a subsidized item, amounting to RM203 million or RM550K per day to Bukhary Sdn Bhd (BSB). The balance unpaid by BSB at end of 2009 was RM118 million or equivalent to 212 days of sales when according to the accounts, normal trade terms was 7 to 90 days.

For 2008, TW sold RM165 million worth of sugar to Bukhary Sdn Bhd and the receivables not collected from Bukhary Sdn Bhd of RM170 million even exceeded the whole year sale of sugar!

I would say it is apparently an excessively favourable treatment by a listed company accorded to a private company belonging to the plc’s controlling interest. As a basic principle, management of a public company must avoid getting into conflict of interest positions.

I am not quite sure what kind of deal the public would be getting from a personality with the above track record. Things can get interesting by the looks of things as per past events...

--------------------------------------------------------------------

http://talkaboutsharesmarket.blogspot.com/2010/06/tradewinds-syed-mokhtar-linked-firms.html

TRADEWINDS: Syed Mokhtar-linked firms’ donations questioned

Tradewinds Plantation Bhd’s (TPB) AGM today could be an interesting affair as the Minority Shareholder Watchdog Group (MSWG) has sent to the company a set of questions ranging from crude oil pricing to a donation of RM10 million made to the Albukhary International University, sources said.

Of particular interest to minority shareholders will be the RM10 million donation, which is deemed as excessive, representing about 20% of the company’s net profit. MSWG’s list of questions also include seeking clarity on its plans to build palm oil mills.

TPB’s 69.76% parent Tradewinds (M) Bhd is also understood to have received a letter from MSWG over its own contribution of RM10 million as well, to the same university. Tradewinds’ AGM is slated for June 22.

The RM10 million contribution by Tradewinds works out to about 12% of its net profit for FY09. Issues have cropped up as Tan Sri Syed Mokhtar Albukhary controls almost 43% of Tradewinds and has an interest in the university as well.

-------------------------------------------------------------------

Is DRB going to raise borrowings of RM622.8 million to make the acquisition? If that is so, then as Pos Malaysia only derive revenue from a public service from Malaysians hence there would be an additional RM622.8 million worth of national debt for all of us to chew on.

If vital national supply and services are concentrated into a few individuals then perhaps ETP stands for Elitist Transfers Programme.

If privatisation is to provide more efficient service then the excellent article below spelt out the less than ideal situation beneath the exciting images portrayed by Pos Malaysia for the past few years.

In addition to the crippling Transmile Group scandal which whacked RM200-RM300 million off the profits of Pos Malaysia, the article also highlighted that its chairman and managing director had resigned over irregularities in land sales and award of contracts.

http://business.feedfury.com/content/17725759-pos-malaysia-new-scandal-after-transmile-irregularities.html

The fact that the chairman and managing director (bumiputras, no less) could only resign* in protest suggested that there were higher powers at work that frustrated & probably prevented capable and honest professionals from taking the necessary corrective action.

This kind of working environment will deter high calibre overseas based Malaysians from coming back. This is more important than the 15% income tax abruptly announced by Najib of which the details have yet to be worked out.

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

*foot note:

Very recently, the chairman took Pos Malaysia and Khazanah to court for breach of chairmanship contract.

http://www.sun2surf.com/article.cfm?id=60169

In the first suit, Adam is suing the Minister of Finance, the government and Pos Malaysia Bhd. In the second suit, which was filed separately, he named Khazanah Nasional Berhad managing director Tan Sri Azman Mokhtar as the defendant.

Adam told Bernama that his suit against Pos Malaysia had been settled amicably after he withdrew his legal action against it about three months ago.

- perhaps Pos Malaysia has to make peace knowing court action may not be advisable for them?

In the suit against Azman filed on Nov 4 last year, Adam alleged that due to unlawful interference by Azman, the government decided to terminate his contract through two letters signed by the Minister of Finance dated May 23 and May 26, 2008 whereas his appointment was supposed to end only on Feb 28, 2009.

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

Yeah sure those are old stories dated 2008 but let's look at the audited accounts for 2010:

Pos Malaysia invested RM7.6 million into 3 associated companies, of which are all wiped out as useless investment, worth RM0. Of the 3, Elpos Print Sdn Bhd earned a revenue of RM12.5 million, but as its liabilities greater than its assets and even whole year's revenue, something is wrong. (Imagine you owe loans and debts which exceed your whole year salary...that is terrifying or down right stupid financial management)

If you look at the notes for related party transactions, Pos Malaysia gave Elpos Print Sdn Bhd RM10 million revenue out of its RM12 million...so how can a small company given a fat contract with a national monopoly can end up being debt ridden up to such a mess?

Elpos Print Sdn Bhd is 60% owned by Econlink Sdn Bhd and Pos Malaysia owns the remaining 40%.

According to Pos Malaysia's website here,

----------------------------------------------------------------------------

http://www.pos.com.my/websitebm/main2.asp?c=/WebsiteBM/subsidiaries/Elpos.htm

Elpos Print Sdn Bhd merupakan salah satu daripada pencetak utama untuk Pos Malaysia Berhad. Elpos ditubuhkan secara perkongsian di antara Pos Malaysia Berhad dan Econlink Sdb Bhd pada tahun 1997.

----------------------------------------------------------------------------

One would expect Pos Malaysia, in awarding what is effectively a public service subcontract, would exercise caution and chosen a reputable party to be prudent with public funds.

A reputable company should exhibit some healthy form of publicity, so as to project a positive image and provide relevant information to advertise itself. Many SMEs have their informative and sometimes interactive website to facilitate ease of business.

Yet, when an attempt to google up this concessionaire, all I get is a scanty picture below:

The company does not own a website, like many SMIs, to let potential customers get to know about basic facts of the company like who are the board of directors, catalogue of their products and services etc. For a company that has been a concessionaire of Pos Malaysia since the last century, surely there should be enough accumulated profits, expertise, track record to be a successful and independent enterprise.

Yet I only see a relatively subdued enterprise named as "pencetak utama" by Pos Malaysia being written off as an investment despite getting a secured and relatively sizeable source of income from Pos Malaysia. It is also contradictory for Pos Malaysia to call it a key supplier and a useless investment simultaneously. Frankly when you are getting a secured, multi-million contract doing printing work for a monopoly cum glc, it is very very hard to run your company into deep shit unless you are supremely unlucky or incompetent.

Sure, in light of the multi million and multi billion ringgit scandals that numb Malaysians into oblivion, the above seems like a small matter but yet, if Pos Malaysia that has been in operations for decades can't even do simple things right, then we can forget about becoming developed nation, Vision 2020, High Income Nation and all the other sales pitch for election

The lastest about Pos Malaysia though, is the disposal of Pos Malaysia by Khazanah to Syed Mokhtar

---------------------------------------------------------------------------

http://www.todayonline.com/Business/EDC110423-0000325/DRB-to-buy-Msian-govts-stake-in-Pos-Malaysia

DRB to buy M'sian govt's stake in Pos Malaysia

04:46 AM Apr 23, 2011

KUALA LUMPUR - DRB-Hicom, a Malaysian automotives, construction and banking group controlled by billionaire Syed Mokhtar Al Bukhary, has won a race to become the biggest shareholder in the Malaysia's national postal company.

It will pay RM622.8 million (S$255.6 million), or RM3.60 per share, for a 32.2-per-cent stake in Pos Malaysia, according to an e-mailed statement by Khazanah Nasional yesterday. That is a 7-per-cent premium to the company's closing share price yesterday of RM3.37.

Khazanah, an investment arm of the Malaysian government, is divesting after Prime Minister Najib Razak called on state organisations to sell down some non-core local commercial holdings to help boost stock market liquidity and attract investment. DRB-Hicom beat four other rival bids which Khazanah did not name in the statement.

----------------------------------------------------------------

In evaluating the bid from various parties, Najib administration awarded the sale to Syed Mokhtar base on the following argument:

"DRB-Hicom was chosen based on their overall bid, which offers not only a defined strategy but also an executable business plan and an acceptable offer price," Mr Azman Mokhtar, managing director of Khazanah....

I have previously written that according to the 2009 audited accounts of Tradewinds (M) Berhad (TW), TW sold sugar, a subsidized item, amounting to RM203 million or RM550K per day to Bukhary Sdn Bhd (BSB). The balance unpaid by BSB at end of 2009 was RM118 million or equivalent to 212 days of sales when according to the accounts, normal trade terms was 7 to 90 days.

For 2008, TW sold RM165 million worth of sugar to Bukhary Sdn Bhd and the receivables not collected from Bukhary Sdn Bhd of RM170 million even exceeded the whole year sale of sugar!

I would say it is apparently an excessively favourable treatment by a listed company accorded to a private company belonging to the plc’s controlling interest. As a basic principle, management of a public company must avoid getting into conflict of interest positions.

I am not quite sure what kind of deal the public would be getting from a personality with the above track record. Things can get interesting by the looks of things as per past events...

--------------------------------------------------------------------

http://talkaboutsharesmarket.blogspot.com/2010/06/tradewinds-syed-mokhtar-linked-firms.html

TRADEWINDS: Syed Mokhtar-linked firms’ donations questioned

Tradewinds Plantation Bhd’s (TPB) AGM today could be an interesting affair as the Minority Shareholder Watchdog Group (MSWG) has sent to the company a set of questions ranging from crude oil pricing to a donation of RM10 million made to the Albukhary International University, sources said.

Of particular interest to minority shareholders will be the RM10 million donation, which is deemed as excessive, representing about 20% of the company’s net profit. MSWG’s list of questions also include seeking clarity on its plans to build palm oil mills.

TPB’s 69.76% parent Tradewinds (M) Bhd is also understood to have received a letter from MSWG over its own contribution of RM10 million as well, to the same university. Tradewinds’ AGM is slated for June 22.

The RM10 million contribution by Tradewinds works out to about 12% of its net profit for FY09. Issues have cropped up as Tan Sri Syed Mokhtar Albukhary controls almost 43% of Tradewinds and has an interest in the university as well.

-------------------------------------------------------------------

Is DRB going to raise borrowings of RM622.8 million to make the acquisition? If that is so, then as Pos Malaysia only derive revenue from a public service from Malaysians hence there would be an additional RM622.8 million worth of national debt for all of us to chew on.

If vital national supply and services are concentrated into a few individuals then perhaps ETP stands for Elitist Transfers Programme.

My EG - where did the My comes from?

MyEG is currently on the roll now. Its financial results are looking good. It looks to provide a positive image to the government's modernization initiative and enable IT savvy Malaysians to handle mundane transactions without needing to travel and queue.

According to Malaysia123.com

MyEG Services Berhad is a concessionaire for the Malaysian E-Government MSC Flagship Application. MyEG role as a Service Provider for the E-Services component essentially provides the electronic link between the Government and citizens/businesses

Through MyEG portal, MyEG offer the Malaysian public a single point of contact between the Government and the people it serves. MyEG portal enables Malaysians to dynamically interact with numerous agencies within the Federal, State and the Local Government machinery providing services ranging from information searches to licence applications.

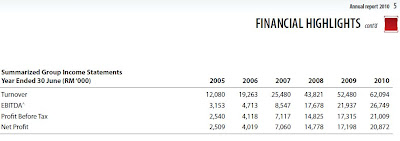

Turnover and profits are on increasing trend for this listed company:

Effectively MyEG is

According to Malaysia123.com

MyEG Services Berhad is a concessionaire for the Malaysian E-Government MSC Flagship Application. MyEG role as a Service Provider for the E-Services component essentially provides the electronic link between the Government and citizens/businesses

Through MyEG portal, MyEG offer the Malaysian public a single point of contact between the Government and the people it serves. MyEG portal enables Malaysians to dynamically interact with numerous agencies within the Federal, State and the Local Government machinery providing services ranging from information searches to licence applications.

Turnover and profits are on increasing trend for this listed company:

Effectively MyEG is

1) given a monopoly of handling e-government transactions; and

According to the annual reports and accounts, the annual pay package of the executive directors is about RM312,000 per year. So with an "s", presumably there is more than 1 executive director hence the RM300K was supposed to be shared out.

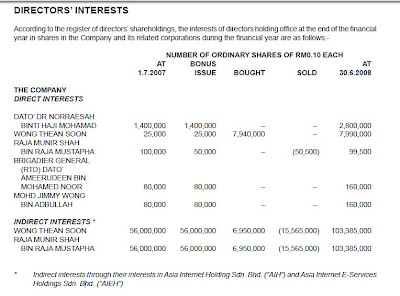

Raja Munir Shah and Wong Thean Soon are designated as Executive Director and Managing Directors respectively in the annual reports so my mind boggles how 2 person can be deemed to control 56 million shares in the company that pays between them, probably around RM300K a year? Most intriguing.

Raja Munir Shah and Wong Thean Soon are designated as Executive Director and Managing Directors respectively in the annual reports so my mind boggles how 2 person can be deemed to control 56 million shares in the company that pays between them, probably around RM300K a year? Most intriguing.

2) given access into private and confidential details of many Malaysians including credit card details, telephone numbers, addresses, traffic summons etc

Why can't the Performance Now administration come up with an inter-ministry/department team to handle this collection function across the administration without a profit element ?(MyEG as a plc needs to generate dividends to its shareholders and guess who is paying for the dividends, plus note 32 of the accounts shows that annually the plc pays about RM200K for rental and professional services to Embunaz Ventures Sdn. Bhd, a company owned by its Executive Chairperson, Dato’ Dr Norraesah Binti Haji Mohamad, "has a substantial financial interest" )

MyEG, to me, seems like another civil service that should be provided to tax payers at no additional cost - i.e. without profit, related party transactions and dividends. Sure theoretically, private enterprise are more efficient than public sector because of the profit motive but I have dealt with Hong Kong and Singapore immigration and income tax departments to know that with the right work attitude and culture, public service can be very very efficient and impressive.

While tax payers in private sector have to deal with risk of business downturn, pay-cuts, voluntary separation schemes, retrenchment, unfair/wrongful dismissals and other threats to our livelihood, majority of civil servants enjoy an iron rice bowl, pension (which offset the disadvantage of lower pay), immunity from disciplinary action (ask Siti Inshah and those BTN indoctrinators), pressure-less environment (unless you are in public schools), no performance yardstick (try calling an ambulance from public hospitals and see what happens) and whatever whatever. Yeah sure, working in public sector has it disadvantages too but certainly not as stressful as those in risk-taking private sector.

Several matters pop into my mind.

Best Bloated Civil Service

With 1.3 million civil servants to a population of 26 million, Malaysia has one of the highest civil servants-to-population ratio in the world by the Organisation for Economic Cooperation and Development standards.

In 2009, Malaysia’s civil servants-to-population ratio was highest in Asia Pacific. Her ratio was 4.68%, compared to Indonesia’s 1.79%, Korea’s 1.85% and Thailand’s 2.06% all of which have less than half our ratio.

In 2009, Singapore had a total of 60,000 civil servants, i.e., 1.5% of the total population. Hong Kong had 160,000 out of a population of 7 million (2.3%). Taiwan(population of 23 million) was served by only 528,000 (2.3%).

So the question is, are Malaysians paying double? Are we still paying for excessive number of civil servants while some of their jobs have been outsourced?

In addition, what kind of clause, terms and conditions did the Barisan Nasional administration bound the rakyat into? As tax payers' surely we have the rights to know. The audited accounts of MyEg merely included the statement:

We can't tell how we are being charged by MyEG, can we? Besides, were there open tenders called to ensure Malaysians got the best deal? Why MyEG was chosen? What are the safety procedures in place to ensure our private and confidential information submitted is not being abused?

We can't tell how we are being charged by MyEG, can we? Besides, were there open tenders called to ensure Malaysians got the best deal? Why MyEG was chosen? What are the safety procedures in place to ensure our private and confidential information submitted is not being abused?

If 1Malaysia -Performance-Now administration can outsource the "accounts receivable" function of JPJ, DBKL, Imigresen etc then how come we Malaysians are saddled with the most bloated civil service around?

Best Bloated Civil Service

With 1.3 million civil servants to a population of 26 million, Malaysia has one of the highest civil servants-to-population ratio in the world by the Organisation for Economic Cooperation and Development standards.

In 2009, Malaysia’s civil servants-to-population ratio was highest in Asia Pacific. Her ratio was 4.68%, compared to Indonesia’s 1.79%, Korea’s 1.85% and Thailand’s 2.06% all of which have less than half our ratio.

In 2009, Singapore had a total of 60,000 civil servants, i.e., 1.5% of the total population. Hong Kong had 160,000 out of a population of 7 million (2.3%). Taiwan(population of 23 million) was served by only 528,000 (2.3%).

So the question is, are Malaysians paying double? Are we still paying for excessive number of civil servants while some of their jobs have been outsourced?

In addition, what kind of clause, terms and conditions did the Barisan Nasional administration bound the rakyat into? As tax payers' surely we have the rights to know. The audited accounts of MyEg merely included the statement:

We can't tell how we are being charged by MyEG, can we? Besides, were there open tenders called to ensure Malaysians got the best deal? Why MyEG was chosen? What are the safety procedures in place to ensure our private and confidential information submitted is not being abused? Why can't the Performance Now administration come up with an inter-ministry/department team to handle this collection function across the administration without a profit element ?(MyEG as a plc needs to generate dividends to its shareholders and guess who is paying for the dividends, plus note 32 of the accounts shows that annually the plc pays about RM200K for rental and professional services to Embunaz Ventures Sdn. Bhd, a company owned by its Executive Chairperson, Dato’ Dr Norraesah Binti Haji Mohamad, "has a substantial financial interest" )

MyEG, to me, seems like another civil service that should be provided to tax payers at no additional cost - i.e. without profit, related party transactions and dividends. Sure theoretically, private enterprise are more efficient than public sector because of the profit motive but I have dealt with Hong Kong and Singapore immigration and income tax departments to know that with the right work attitude and culture, public service can be very very efficient and impressive.

While tax payers in private sector have to deal with risk of business downturn, pay-cuts, voluntary separation schemes, retrenchment, unfair/wrongful dismissals and other threats to our livelihood, majority of civil servants enjoy an iron rice bowl, pension (which offset the disadvantage of lower pay), immunity from disciplinary action (ask Siti Inshah and those BTN indoctrinators), pressure-less environment (unless you are in public schools), no performance yardstick (try calling an ambulance from public hospitals and see what happens) and whatever whatever. Yeah sure, working in public sector has it disadvantages too but certainly not as stressful as those in risk-taking private sector.

If there is a really 1Malaysia thingy, then the civil servants should buck up, provide satisfactory services to Malaysians and benchmark against service level of Singapore and Hong Kong; the most efficient around the world.

Disclosure requirements that listed companies must follow, according to accounting standards, company law and Bursa listing requirements, are suppose to give more relevant information for investing public to understand the company they have or thinking of investing in.

Disclosure requirements that listed companies must follow, according to accounting standards, company law and Bursa listing requirements, are suppose to give more relevant information for investing public to understand the company they have or thinking of investing in.

According to the annual reports and accounts, the annual pay package of the executive directors is about RM312,000 per year. So with an "s", presumably there is more than 1 executive director hence the RM300K was supposed to be shared out.

Raja Munir Shah and Wong Thean Soon are designated as Executive Director and Managing Directors respectively in the annual reports so my mind boggles how 2 person can be deemed to control 56 million shares in the company that pays between them, probably around RM300K a year? Most intriguing.

Raja Munir Shah and Wong Thean Soon are designated as Executive Director and Managing Directors respectively in the annual reports so my mind boggles how 2 person can be deemed to control 56 million shares in the company that pays between them, probably around RM300K a year? Most intriguing.

The profile of Raja Munir Shah included the following:

In 1997, he was elected to head the Tanjong UMNO Youth Division and subsequently appointed as the State UMNO Youth Information Chief until his tenure ended in 2004. He was appointed as a City Councilor in 1997, 1998, 2003 and 2004. During his tenure as a Councilor in Penang Island Municipal Council (“MPPP”), he served as Chairman and Committee Member in various standing committees overseeing legislatives and policy matters within the jurisdiction of MPPP which covers the island of Penang.

I have to put my hands up in awe.

But the biggest shock is still to come....

http://sahamas.net/forum80/13150.html

Under the customs tax monitoring scheme, MyEG has a 40% stake in a special purpose vehicle (SPV) that will link up point-of-sales (POS) terminals of businesses that are subject to customs’ service taxes, such as restaurants and entertainment outlets.

The SPV will spend RM100 million on capex, but will receive a 20% share of the taxes that were previously found to be under-declared, with the lion’s share of 80% going to the government.

This will give MyEG a potentially large wildcard from FY June 2013 onwards. However, it is too preliminary to assess at this juncture, as much depends on how much tax was under-declared in the first place. The service will also be compatible with a GST regime that is likely to be implemented at a later stage, giving the company a potentially wider earnings base.

What kind of irresponsible government would

1) let a private sector to help them chase after tax evaders - do you see IRB employing debt collectors? If the custom authorities have an act to enforce, they should just enforce it without additional expebse!

2) let a plc to gobble up to 20% of public's money? these money could be used for welfare, education, healthcare, public utilities etc instead of dividends, private profits etc.

And this path to money printing encompass service, sales taxes and in future, after getting re-elected, GST. The magnitude of benefit coming to MyEG's way, at public's expense, is presently incalculable.

Is it too little and too many tar roads in Sarawak?

My car's road tax is expiring soon and so is the coming of Sarawak GE.

The other day, I picked up the following information from YB Teo Nie Ching's blog:

Sabah & Sarawak possess 60% of land mass of the country but length of tar road is only 6,390km while West M'sia has 21,589km length of tar road

I also chanced upon the audited accounts of UBG Berhad coincidentally.

UGB Berhad has a 15 years road maintenance concession granted by the Sarawak State Government with effect from 1 January 2003 to maintain 4,600km of roads in the state. Given YB Teo's disclosure that there is only 6,390km of tar roads in Sarawak and Sabah, this Road Maintenance Agreement probably granted this happy listed company a monopoly of road maintenance for the entire state.

Revenue recognition policy for this business segment as disclosed in UGB's accounts is"fixed rates subject to revision in accordance with the agreement".

When it is fixed, it is suppose to be fixed. If it is subject to revision then is there an incentive for the concessionaire to keep tight cost control and prevent cost overrun? How hard or how easy is it for the concessionaire to get the rates revised? If abused, this is as good as a profit guarantee or blank cheque. Who approved this Road Maintenance Agreement to be signed with UGB Berhad? Was this tabled and deliberated in the state assembly then?

When it is fixed, it is suppose to be fixed. If it is subject to revision then is there an incentive for the concessionaire to keep tight cost control and prevent cost overrun? How hard or how easy is it for the concessionaire to get the rates revised? If abused, this is as good as a profit guarantee or blank cheque. Who approved this Road Maintenance Agreement to be signed with UGB Berhad? Was this tabled and deliberated in the state assembly then?

Does this look like the equivalent of Semenanjung's ever controversial, very politicalized, profit guaranteeing, inflation-inducing toll highways? Before we even contemplate how much money UGB is making out of this deal, I remember in my form 6 economics class, my dear teacher Puan C. (I still remember your full name, cikgu) taught us that theoretically government collect taxes, taxes are used for providing public goods and it is of the interest of the people that such services are provided without profit-motive.

Let's have a look at the numbers in 2009 and 2008. For these 2 years alone, RM76million gross profit was earned from maintaining the roads. These "profits" I suppose were paid from taxes and instead of being channelled back to building new roads, further repairs and improvement of roads, have been channelled into hands of a plc, which may have become dividends, directors' remuneration (including retirement benefits) etc.

That RM242,593,000 worked out to be RM26,369 per year per km. Sounds like Sarawakians have the best tar roads and pavement in the world. Being a Semenanjungite, I really do not know for very sure.

On 12 May 2009, UGB sold the 2 subsidiary companies for road maintenance and pavement for a combined amount of RM75 million, instant cash generation to the holding company, to its other subsidiary Putrajaya Perdana Berhad. A simple case of left pocket to right pocket.

On 12 May 2009, UGB sold the 2 subsidiary companies for road maintenance and pavement for a combined amount of RM75 million, instant cash generation to the holding company, to its other subsidiary Putrajaya Perdana Berhad. A simple case of left pocket to right pocket.

As Putrajaya Perdana Berhad is aggressively creating prominent landmarks in Semenanjung, I do wonder if the collection of road maintenance revenue in Sarawak can be re-invested back into Sarawak.

It is also interesting to note Mr Low Taek Jho joined Putrajaya Perdana Berhad as an advisor (and I have a hard time understanding what "Non-Independent Non-Executive" means).

All said and done, I notice among the domineering shareholder of Putrajaya Perdana Berhad includes Cahya Mata Sarawak Berhad, a company linked to the current chief minister which makes me wonder if Sarawak is not big enough for him. A partnership of Mr Low and Chief Minister Taib could prove to be redoubtable political-economic tie up.

So if UMNO did not cross over to Sarawak as they did to Sabah, Sarawak's finest export to Semenanjung seems to include Tan Sri Ting Pek Khing and Cahya Sarawak via Putrajaya Perdana Berhad then.

The other day, I picked up the following information from YB Teo Nie Ching's blog:

Sabah & Sarawak possess 60% of land mass of the country but length of tar road is only 6,390km while West M'sia has 21,589km length of tar road

I also chanced upon the audited accounts of UBG Berhad coincidentally.

UGB Berhad has a 15 years road maintenance concession granted by the Sarawak State Government with effect from 1 January 2003 to maintain 4,600km of roads in the state. Given YB Teo's disclosure that there is only 6,390km of tar roads in Sarawak and Sabah, this Road Maintenance Agreement probably granted this happy listed company a monopoly of road maintenance for the entire state.

Source: Annual report and accounts of UGB Berhad for 2009

Source : Annual Report and Accounts of Putrajaya Perdana Berhad, 2009

Revenue recognition policy for this business segment as disclosed in UGB's accounts is"fixed rates subject to revision in accordance with the agreement".

When it is fixed, it is suppose to be fixed. If it is subject to revision then is there an incentive for the concessionaire to keep tight cost control and prevent cost overrun? How hard or how easy is it for the concessionaire to get the rates revised? If abused, this is as good as a profit guarantee or blank cheque. Who approved this Road Maintenance Agreement to be signed with UGB Berhad? Was this tabled and deliberated in the state assembly then?Does this look like the equivalent of Semenanjung's ever controversial, very politicalized, profit guaranteeing, inflation-inducing toll highways? Before we even contemplate how much money UGB is making out of this deal, I remember in my form 6 economics class, my dear teacher Puan C. (I still remember your full name, cikgu) taught us that theoretically government collect taxes, taxes are used for providing public goods and it is of the interest of the people that such services are provided without profit-motive.

Let's have a look at the numbers in 2009 and 2008. For these 2 years alone, RM76million gross profit was earned from maintaining the roads. These "profits" I suppose were paid from taxes and instead of being channelled back to building new roads, further repairs and improvement of roads, have been channelled into hands of a plc, which may have become dividends, directors' remuneration (including retirement benefits) etc.

That RM242,593,000 worked out to be RM26,369 per year per km. Sounds like Sarawakians have the best tar roads and pavement in the world. Being a Semenanjungite, I really do not know for very sure.

On 12 May 2009, UGB sold the 2 subsidiary companies for road maintenance and pavement for a combined amount of RM75 million, instant cash generation to the holding company, to its other subsidiary Putrajaya Perdana Berhad. A simple case of left pocket to right pocket.

On 12 May 2009, UGB sold the 2 subsidiary companies for road maintenance and pavement for a combined amount of RM75 million, instant cash generation to the holding company, to its other subsidiary Putrajaya Perdana Berhad. A simple case of left pocket to right pocket.As Putrajaya Perdana Berhad is aggressively creating prominent landmarks in Semenanjung, I do wonder if the collection of road maintenance revenue in Sarawak can be re-invested back into Sarawak.

It is also interesting to note Mr Low Taek Jho joined Putrajaya Perdana Berhad as an advisor (and I have a hard time understanding what "Non-Independent Non-Executive" means).

All said and done, I notice among the domineering shareholder of Putrajaya Perdana Berhad includes Cahya Mata Sarawak Berhad, a company linked to the current chief minister which makes me wonder if Sarawak is not big enough for him. A partnership of Mr Low and Chief Minister Taib could prove to be redoubtable political-economic tie up.

So if UMNO did not cross over to Sarawak as they did to Sabah, Sarawak's finest export to Semenanjung seems to include Tan Sri Ting Pek Khing and Cahya Sarawak via Putrajaya Perdana Berhad then.

Un-tolled joy or un-told joy?

The Star with its 29th January 2010 headline screamed "un-tolled" joy.

The sentence "no compensation for the 3 highways" makes me wonder. The profit above would have included the compensation for 2009. If the purchase consideration exceeded the profits then the compensation would have been included in the RM3.525 billion anyway.

------------------------------------------------------------------------------

http://www.starproperty.my/PropertyScene/PropertyNews/9896/0/0

Toll abolished on one stretch, no rates hike on two highways

PUTRAJAYA: Toll for the Salak to Taman Connaught stretch of the East-West Link Expressway is set to be abolished by May, Datuk Seri Najib Tun Razak announced.

The Prime Minister also announced that the toll rates for the Kuala Lumpur-Karak Expressway and East Coast Expressway Phase One would not be increased for the next five years.

He said the decisions were made following a review of transportation costs, including restructuring the toll charges and to ease the people’s burden.

He also added that no compensation would be paid to the concessionaires of the three highways.

“In line with the 1Malaysia spirit, People First, Performance Now, I have asked toll concessionaires to carry out a review of the respective toll charges to help the Government prosper the country and lessen the burden of the people.

“Taking up the Government’s call, two corporate figures who are also major shareholders of a toll concessionaire, came forward with a toll restructuring proposal through the acquisition of assets, which will benefit the people,” he told a press conference at his office here yesterday.

Also present was Works Minister Datuk Shaziman Abu Mansor

-------------------------------------------------------------------------------------

An early nice Chinese New Year surprise for the toll hating Chinese community before Tenang by-election?

MTD Capital Berhad operates the above 2 tolled highway until 2032 with another one (not acquired by the directors in this exercise) until 2018.

Below is a screen shot of the letter of offer, announced by MTD Capital Berhad in Corporate Announcement section of the Bursa's website as required by the listing requirements.

According the the offer above, the 2 directors via a Special Purpose Vehicle will pay MTD RM3.525 billion in cash to buy the 2 concessions. I get a bit worried whenever I see the term SPV and any government linked initiative in the same article. Not sure why.

The question is, how is this SPV (i.e. entirely new company, starting from zero) going to raise the RM3.525 billion? Is it from bank loan guaranteed by government? Government loan? EPF investment? Khazanah contribution? Either way, the rakyat is going to finance this either via tax money or hard earned deposits with commercial banks. It looks unlikely that some rich entrepreneur came up with the cash elsewhere.

The challenge nowadays is to achieve more with less resource; not achieve less with more resource committed. So is this a good deal for the people as the Prime Minister indicated?

This is tricky as I do not have all the relevant details. According to MTD Capital Berhad's 2009 audited accounts, 3 tolls gave them a profit before finance charges and tax of RM143.8 million

Now this RM143.8 million is from 3 toll highways but in the absence of the breakdown per highway, I took the offer purchase price of RM3.525 billion for 2 highway toll concessions and divided by total profit earned by 3 concessions.

Lo and behold, it is about 24 1/2 years, calculating from 2011 onwards, it covers profits up to 2035 while the 2 concessions will end July and December 2032. 3 years extra.

Those who understand financial terminology knows what I am saying - I do not have MTD's WACC nor cash flow projection to do a proper discounting.

From tax payers' point of view, why can't Najib administration negotiate better? By paying off immediately, the termination of business risk and immediate cash inflow would worth a huge discount from MTD. If Rakyat Diutamakan surely the most powerful prime minister can play a bit of hard ball and carrot & stick to part with lesser money? He has proven to be a smooth political plotter elsewhere.

Although the article mentioned no increase for 5 years, there is no further details about whether the length of concession will remain the same or otherwise, nor what will happen from the 6th year onwards.

Furthermore, who are the shareholders of the SPV? To whom the profits arising from future toll be going to? Does the SPV have concrete cost management and reduction programme? Is there going to be open tender by the SPV to obtain the best offers from vying contractors to maintain the highway?

The sentence "no compensation for the 3 highways" makes me wonder. The profit above would have included the compensation for 2009. If the purchase consideration exceeded the profits then the compensation would have been included in the RM3.525 billion anyway.

I won't be jumping with un-tolled joy until the untold parts are clear to me.

PLUS EXPRESSWAY : Scratching the tip of a block of tar

The biggest deal for the year so far is of course the UEM-EPF acquisition of PLUS. Without DAP Economic Bureau's alternative budget for 2010 proposing a RM15 billion bid to nationalise PLUS, I doubt if this UEM-EPF initiative would ever be mooted by the BN administration.

-------------------------------------------------------------------------------

http://biz.thestar.com.my/news/story.asp?file=/2011/1/18/business/7818903&sec=business

Tuesday January 18, 2011

PLUS Expressways says UEM-EPF offer ‘confirmed’

PETALING JAYA: PLUS Expressways Bhd's board of directors, save for the interested directors, has deemed the UEM Group Bhd-Employees Provident Fund's (EPF) RM23bil takeover offer as a “confirmed offer.”

It told Bursa Malaysia yesterday that the board had decided to proceed with the adjourned EGM for its non-interested shareholders to consider the disposal of its entire business and undertaking to UEM-EPF, and the proposed distribution of the cash proceeds to all entitled shareholders via a proposed special dividend and selective capital repayment.

----------------------------------------------------------------------------------------

So under BN, the valuation is RM8 billion more than DAP's economic bureau but that is not what I am examining here.

I took a look at the 2009 audited accounts and try to appreciate the magnitude of the issue at hand.

-------------------------------------------------------------------------------

http://biz.thestar.com.my/news/story.asp?file=/2011/1/18/business/7818903&sec=business

Tuesday January 18, 2011

PLUS Expressways says UEM-EPF offer ‘confirmed’

PETALING JAYA: PLUS Expressways Bhd's board of directors, save for the interested directors, has deemed the UEM Group Bhd-Employees Provident Fund's (EPF) RM23bil takeover offer as a “confirmed offer.”

It told Bursa Malaysia yesterday that the board had decided to proceed with the adjourned EGM for its non-interested shareholders to consider the disposal of its entire business and undertaking to UEM-EPF, and the proposed distribution of the cash proceeds to all entitled shareholders via a proposed special dividend and selective capital repayment.

----------------------------------------------------------------------------------------

So under BN, the valuation is RM8 billion more than DAP's economic bureau but that is not what I am examining here.